By Leonie Hartmann | Updated on: February, 2026 | 🕓 15 minutes read

Key Highlights

- What are digital nomad visas really offering: freedom or fiscal risk?

- How do visa rules differ from tax residency requirements?

- What hidden obligations could affect both you and your employer?

- How to assess and mitigate permanent establishment and social security risks?

- Practical steps to build a mobility framework for long-term nomadic work.

Who Should Read This: Individuals with existing remote income who are considering or already hold a digital nomad visa—this is not a beginner's guide on "how to become a digital nomad," but a clear-headed handbook for those already on the road.

1. A Carefully Packaged Narrative Trap

Imagine this scenario:

You spend three months preparing documents, pay a $500 application fee, and finally receive a digital nomad visa for a certain country. The visa officer smiles and tells you, "Remote workers are tax-exempt—enjoy your life." Six months later, you receive a letter from the local tax authority requesting that you declare your worldwide income and pay social security contributions. You are stunned—the visa officer clearly told you it was tax-free.

This is not fiction. It happened in 2024 to an American developer in Portugal. He held a D8 digital nomad visa and stayed eight months in Portugal, assuming he was still covered under the NHR (Non-Habitual Resident) tax benefits. What he didn’t know was that the NHR program officially ended in January 2024, and the new IFICI regime effectively closed the door for "ordinary remote workers." In the end, his effective tax burden reached 70%—48% progressive income tax, 5% solidarity surcharge, and 21% self-employment social contributions.

The popularity of digital nomad visas is essentially a tourism department KPI product, not a system designed or endorsed by tax authorities. This "departmental wall" creates information gaps—the source of most of these traps.

Grant Thornton’s review of 21 countries found that 79% of digital nomad visas do not provide personal income tax exemptions, and 85% do not provide corporate tax risk exemptions. In other words, when you enter a country with a visa, you have permission from the immigration office—but the finance ministry may not recognize it at all.

2. First Layer of Trap: Visa ≠ Tax Residency—What You Think Is “Legal Residence” Might Be “Tax Naked”

2.1 The Parallel Universe of Visa and Tax Residency

A visa is permission from the immigration office; tax residency is a determination by the finance authority—they operate independently. Understanding this is the prerequisite for avoiding all traps.

Most countries use the 183-day rule to determine tax residency: staying more than 183 days within a calendar year or consecutive 12 months makes you a tax resident, liable for worldwide income tax. Ironically, many digital nomad visas are deliberately designed for 180 days + extendable, perfectly sitting on the red line of tax residency.

Thailand’s DTV visa is a textbook example. It allows a stay of 360 days, but Thai tax law may recognize you as a tax resident if you stay over 180 days. Officials provide zero clarification—immigration issues the visa without warning, and the tax office does not proactively explain. You only learn when a tax bill lands in your mailbox.

Even subtler is the difference in day-counting methods. The U.S. IRS, when applying the Physical Presence Test, does not count entry or exit days as full days; many European and Asian countries do count. This means the 183 days you track yourself may differ from the tax authority’s calculation.

2.2 Hidden Tax Residency Triggers

Center of Economic Interest Test: Even if you stay less than 183 days, if your main clients, bank accounts, and contract locations are in that country, you can still be deemed a tax resident. A German freelance designer living five months in Croatia with mostly local clients was classified as a tax resident, despite not meeting the day threshold.

Presumption of Permanent Home: Rental contracts, local phone numbers, gym memberships, even a library card—these lifestyle markers can serve as evidence of "residential intent" in audits. A British remote worker in Spain was audited, with the tax office presenting his 12 months of gym membership payments as proof of a permanent home.

2.3 The Special Case for U.S. Citizens

If you hold a U.S. passport, the situation is more complicated. The United States taxes global income, and most tax treaties include a Saving Clause, allowing the U.S. to retain taxing rights on citizens even when a treaty suggests otherwise.

Many American nomads rely on FEIE (Foreign Earned Income Exclusion) to reduce their tax burden, but FEIE has a hidden requirement: you must establish a "Foreign Tax Home." If you move between countries every three months, the IRS may deem your tax home still in the U.S., invalidating your FEIE.

One American freelance writer hopping between islands in Southeast Asia for two years had their FEIE claim denied in 2023, because they "lacked a substantial connection to any single foreign tax home." They ultimately paid over $40,000 in back taxes and penalties for two years.

3. Second Layer of Trap: Your “Freedom” Is Creating Risk for Your Employer

3.1 Permanent Establishment (PE) Risk—You Are Not Alone

Working remotely for a company abroad may create a Permanent Establishment (PE) in that country for your employer.

PE has serious consequences: the employer’s global profits could be taxed in the host country, and they may have to contribute to local social security. This is not hypothetical—2023 saw a U.S. SaaS company deemed to have a PE in South Africa because an employee worked remotely there for over six months, resulting in over $800,000 in taxes and penalties.

South Africa is particularly notable. Even without PE, foreign employers may need to pay unemployment insurance (UIF) and skills development taxes (SDL) for remote employees—creating a surreal situation of "obligations without rights." A Canadian developer with a South African digital nomad visa discovered their U.S. employer refused to continue employment because HR systems couldn’t handle this “obliged but powerless” setup.

3.2 Why 90 Days Is a Red Line for Most Companies

Companies like Airbnb, Shopify, and Wise impose "90-day overseas work" policies not out of caution but as the best compromise for tax compliance. Beyond 90 days, HR systems often cannot handle multi-jurisdictional payroll, social contributions, and equity tax. A product manager at Wise said the company system doesn’t even list "digital nomad visa" as an option—if you’re outside standard countries, the default is that you cannot be legally paid.

3.3 The “Pseudo-Independence” Trap for Freelancers

Many freelancers create a personal company (e.g., Estonia OY, UK Ltd) to contract themselves and then apply for a foreign employer visa as an "employee." In countries like South Africa, this can trigger corporate tax residency, meaning the personal company is treated as doing business locally and subject to corporate tax.

Even more hidden is double social security contributions. Without a Totalization Agreement, you may pay full social security to both your home and host countries. A freelance developer in Spain with an Australian passport paid over 35% of income in combined social contributions, while no agreement existed between the two countries.

4. Third Layer of Trap: Structural Exploitation Built into Visa Design

4.1 Who Bears the Cost of Whose Fiscal Deficit?

The real economic model of digital nomad visas is clear: attract high-spending foreigners without occupying local jobs, while not providing equivalent social benefits.

Consider the thresholds:

- Thailand DTV: 500,000 THB (~$14,500) deposit + visa fee

- UAE Green VisA: University degree or minimum monthly salary 15,000 AED (~$4,000)

- Costa Rica RentistA: Minimum passive income $2,500/month

These requirements screen not for "top talent," but for financially cushioned cash cows. You are allowed to consume, rent, eat, and drink coffee—but cannot vote, access public healthcare, or claim unemployment benefits. You inject foreign currency into the local economy, but bear all risks yourself.

4.2 Service Vacuums: You Bought a Ticket, But Nobody Cares Once You Board

Thailand DTV bureaucratic lottery: Approval rates vary drastically between consulates. Some receive approval in three days in Bangkok; others are rejected twice in Los Angeles due to “income proof format” issues—with no official guideline. There is no appeal mechanism.

Banking paradox: The visa grants "resident status," but banks still consider you a "tourist." A Brazilian developer in Croatia with a digital nomad visa tried five banks but was denied personal accounts, being forced to use a Brazilian credit card paying 3% cross-border fees and poor exchange rates.

Extension roulette: DTV promises six-month extensions, but some immigration offices reject them outright without standards. A French designer in Chiang Mai whose extension was rejected had only 14 days to exit the country, paying one-third of a month’s income for a last-minute flight to Vietnam.

4.3 Local Community Backlash

The low-cost advantage for nomads comes at a cost to locals.

Lisbon, Portugal: From 2019–2024, one-bedroom apartment rents in the city center rose over 120%. Local youth launched the " StopDigitalNomads" campaign, blaming remote workers for housing inflation.

Mexico City, Mexico: Roma Norte cafes switched to English menus; long-time local customers felt excluded. A Mexican writer wrote, "Our community has become their theme park."

This tension is pushing governments to tighten policies. From “welcoming nomads” to “regulating nomads”—in 2025, Portugal started discussing a “housing impact fee” for digital nomads; some Italian cities now require proof that visa applicants “will not worsen local housing scarcity.”

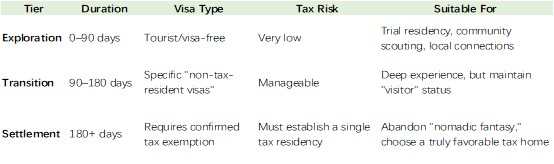

5. Fourth Layer: Real “Anti-Fragility” Strategy—Not Finding the Perfect Visa, But Building a Mobility Framework

5.1 From “Visa Hunting” to “Tax Architecture Thinking”

Stop looking for a "perfect visa." It doesn’t exist. Instead, build a three-tier mobility model:

Key principle: In exploration and transition tiers, the goal is not triggering tax residency; in settlement, the goal is actively choosing a favorable tax home, rather than being passively "caught" by a country.

5.2 Four-Quadrant Visa Evaluation

Evaluate any digital nomad visa along two dimensions:

Decision logic: Prioritize the "explicit exemption" quadrant; avoid "no exemption + high tax" death combination.

5.3 Practical: Pre-Application “Five-Step Due Diligence”

Do not trust visa websites claiming “tax-friendly.” Conduct these five steps yourself:

Step 1: Review the tax code directly

Search "[Country] tax code non-resident visa holder" or "[Country] income tax act Article X." Find specific article numbers, not website summaries.

Step 2: Check social security agreements

Search for Totalization Agreements between your home and target country. U.S. citizens can check SSA lists; EU citizens have A1 certification; others require bilateral verification.

Step 3: Verify banking policies

Don’t ask an agent, “Can I open an account?” Email three local banks: “Can I open a personal account with a [Visa Name]?” Keep written replies as evidence.

Step 4: Check extension history

Search Reddit for “visa extension denied [Country]” or Facebook for “[Country] digital nomad visa extension.” Review real rejections, not success stories.

Step 5: Assess PE risk

If employed, ask your employer’s tax advisor: “If I work from [Country] for 6 months, does the company risk creating a Permanent Establishment?” If the answer is "probably fine" without citing specific law, they haven’t done proper research.

5.4 Build a “Mobility Emergency Kit”

Tax Document Cloud: Archive all entry stamps, rental agreements, bank statements, and contracts by year and country. Recommended: encrypted cloud + local backup.

Day Tracker: Do not rely on “rough memory.” Use TravelSpend to record every entry/exit, export weekly to Excel, set a 183-day warning. Update weekly, not monthly.

Professional Advisor White List: Contact two English-speaking tax lawyers in target countries ahead of time (lawyers, not accountants, due to confidentiality). Written advice costs $200–500, potentially saving tens of thousands in unexpected taxes.

Conclusion: Digital Nomad Visas Are Not an Endpoint, But a Stress Test

The true value of a digital nomad visa is not the romantic notion of "living elsewhere," but low-cost testing of whether a jurisdiction is worth long-term commitment. Treat it like a "trial marriage," not a "flash wedding."

Tax incentives are policy—they change. Doors open today may close tomorrow. Real freedom is not where you can go, but knowing what you face when you go. The biggest trap of digital nomad visas is making you think that once the paperwork is done, you are free. In reality, the paperwork is just the beginning of the real game.

Appendix: High-Value Resources and Glossary

Official Tools

- OECD Tax Residency Tool (OECD Model Tax Convention)

- IRS Foreign Earned Income Exclusion (FEIE) Eligibility Tests (U.S. Citizens only)

- National tax authorities’ “Non-Resident Tax Guides” (always more accurate than visa websites)

Community Validation

- Nomad List Tax forum discussions

- Country-specific Facebook groups (e.g., "Americans in Portugal," "Digital Nomads in Thailand")

- Reddit r/digitalnomad filtered by "Tax"

Key Terms

- FEIE: Foreign Earned Income Exclusion (U.S.)

- PE: Permanent Establishment

- DTA: Double Taxation Agreement

- Totalization Agreement: Social security exemption agreement

- Tax Home: Determination of tax residency for FEIE eligibility (IRS standard)

FAQs

Q1: Do digital nomad visas automatically exempt me from income tax?

A: No. A digital nomad visa is primarily issued by immigration authorities and does not guarantee any tax exemption. Most countries treat tax residency separately from visa status, and many digital nomad visas do not provide explicit income tax or corporate tax exemptions. Always check the host country’s tax code directly.

Q2: How can I determine my tax residency while moving between countries?

A: Tax residency is usually determined by factors like physical presence (e.g., 183 days rule), center of economic interest, or evidence of a permanent home. Even if you hold a short-term visa, signing leases, opening local bank accounts, or working for local clients may trigger tax residency. Check local tax law and, if needed, consult a tax professional.

Q3: What is a Permanent Establishment (PE), and how could it impact my employer?

A: A PE arises when your presence in a foreign country is considered as creating a local office or business for your employer. This could require your employer to pay corporate tax, social security, or other obligations in that country. If your company is unaware, it can lead to substantial fines. Employers often limit overseas work to 90 days to mitigate PE risk.

Q4: Are there countries that clearly provide tax exemptions for nomads?

A: Yes, but they are rare. Some countries like Croatia, Uruguay, or certain regimes in Portugal and Spain provide explicit tax benefits for long-term residents or non-habitual residents. Always verify via official tax codes or consult a local tax lawyer, as policies can change quickly.

Q5: How can I verify banking, extension, and social security rules before applying for a visa?

A: Conduct a five-step due diligence before applying:

1. Read the original tax law for non-resident or special visa holders.

2. Check for social security agreements (Totalization Agreements) between your home and host country.

3. Email local banks to confirm account opening rules for your visa type.

4. Research visa extension success/failure cases in forums and Facebook groups.

5. Discuss PE risks with your employer’s tax advisor and request written clarification.

References

1. Grant Thornton. (2024). Global Digital Nomad Visa Review: Tax and Regulatory Implications. Grant Thornton International. [https://www.grantthornton.global/]

2. OECD. (2023). Model Tax Convention on Income and on Capital. Organisation for Economic Co-operation and Development. [https://www.oecd.org/tax/treaties/]

3. U.S. Internal Revenue Service (IRS). (2023). Foreign Earned Income Exclusion (FEIE) and Tax Home Guidelines. [https://www.irs.gov/]

4. Reddit r/digitalnomad. (2024). Tax Discussions. [https://www.reddit.com/r/digitalnomad/]

5. Nomad List. (2024). Digital Nomad Visa and Tax Experiences. [https://nomadlist.com/]

About the Author

Leonie Hartmann

Leonie Hartmann is a migration policy writer and cross-border labor researcher specializing in temporary migration systems, international labor mobility, and visa-driven employment markets. Her research explores how governments, employers, and private consulting industries influence migration pathways for students, skilled workers, and digital nomads. Leonie frequently writes about immigration consulting practices, labor shortages, visa sponsorship structures, and the economic realities behind modern migration narratives. Her work combines policy analysis with practical insights for globally mobile professionals.

Editorial Transparency Statement

This article was independently researched and written without sponsorship from any visa or tax advisory firm. Sources include publicly available tax law, government websites, and verified community experiences. No affiliate links or promotional content influence the recommendations or analysis.

Disclaimer

This article is for general informational purposes only. It does not constitute tax, legal, or immigration advice. Laws and regulations may change, and personal circumstances vary. Before making any decisions about visas, taxation, or cross-border employment, consult a licensed tax advisor or immigration lawyer. The author and publisher assume no responsibility for outcomes arising from the use of this information.