By Marco Elian Ruiz | Updated on March, 2026 | 🕓 15 minutes

Key Highlights

- Why are digital nomads increasingly being audited by multiple countries at the same time?

- What is a “tax residency certificate,” and why do banks now demand it?

- Could your remote work apartment accidentally create a permanent establishment (PE) for your company?

- What is an exit tax, and why can it create a six-figure tax bill before you even leave your home country?

- Which countries are commonly chosen by digital nomads as primary tax residency bases?

- What practical steps can help reduce international tax residency conflicts?

1. Sarah’s Story: When “Tax Freedom” Turns Into a Tax Nightmare

At the beginning of 2024, Sarah — an independent software consultant from Vancouver — made what seemed like the perfect decision.

She sold her condo, canceled her Vancouver gym membership, stored her furniture in her parents’ basement, and bought a one-way ticket to Mexico City. Her plan was simple: spend four months in Mexico City, then four months in Lisbon, and finally four months in Chiang Mai. She believed that as long as she stayed under 183 days in every country, she would become “tax free.”

She was wrong.

In February 2025, Sarah received three letters at the same time.

The first came from the Canada Revenue Agency (CRA), informing her that because she had not fully severed her residential ties with Canada, she was still considered a Canadian tax resident and had to pay tax on her worldwide income for 2024.

The second came from the Portuguese tax authority, stating that the apartment she rented in Lisbon and her local bank account constituted a “permanent home,” requiring her to declare income earned during her stay in Portugal.

The third came from her bank, demanding that she provide valid proof of tax residency within 30 days or risk having her account frozen.

What devastated her most was a number mentioned in the Canadian letter: because she held approximately CAD 500,000 in publicly traded stocks and CAD 200,000 in private company shares, Canada deemed that she had “disposed” of all her assets at fair market value on the day she left the country. Fifty percent of the capital gains became taxable income.

Before she had even boarded her flight to Mexico, she already owed a six-figure departure tax.

This is not a fictional story. It is a recurring scenario in international tax consulting.

According to a 2023 report by the United Nations Committee of Experts on International Cooperation in Tax Matters focusing on digital nomad taxation, cases like Sarah’s are increasing rapidly worldwide.

And the mistake Sarah made is exactly the same mistake most digital nomads make:

She thought she was playing a “days game.” Tax authorities are playing a “connections game.”

2. Trap One: The 183-Day Rule — The Biggest Misconception Among Digital Nomads

If you search online for “digital nomad tax residency,” 99% of articles will tell you the same “safe rule”:

Stay under 183 days in every country, and you won’t become a tax resident.

That advice is not only oversimplified — for most digital nomads, it is fundamentally unreliable.

Why the 183-Day Rule Is Not Your Shield

The 183-day rule originates from the OECD Model Tax Convention. It was originally designed to solve taxation issues for traditional expatriate employees — for example, a German engineer temporarily assigned to France for six months.

It was never designed for people carrying laptops around the world while working remotely for clients in multiple countries.

More importantly, countries calculate “183 days” in completely different ways:

- Calendar-year basis: January 1 to December 31 (used by most countries)

- Rolling 12-month basis: Thailand, for example, may count any consecutive 12-month period exceeding 180 days

- Weighted multi-year calculation: The United States uses the “Substantial Presence Test,” which weights your physical presence over the previous three years using a 1 : 1/3 : 1/6 formula. You may spend only 120 days in the U.S. during one year, but still trigger tax residency once prior years are included

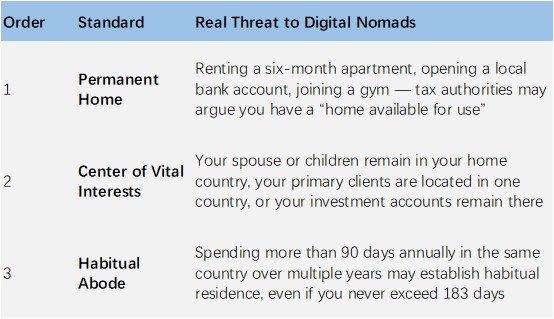

The Real Danger: Three Invisible Red Lines

Article 4 of the OECD Model Tax Convention introduces the “tie-breaker rules.” When two countries may both claim you as a tax resident, they generally evaluate the following factors in order:

A Real Example

A German designer spent approximately five months per year in Barcelona from 2022 to 2024. He carefully stayed under the 183-day threshold each year.

In early 2025, Spanish tax authorities determined that he had established a habitual abode in Spain and demanded back taxes and penalties on his worldwide income for those years.

His “183-day strategy” completely failed.

Self-Assessment: How Complicated Is Your “Tax Connection Map”?

Take five minutes and answer these questions. If multiple answers point to the same country, that country may still argue that you are a tax resident — even if you only stayed there for 100 days.

〇 In which country do I maintain bank or investment accounts?

〇 Where do my spouse/partner or minor children live?

〇 In which country do I own property, even if rented out?

〇 Where are my primary clients or employer located?

〇 In which country is my company or business entity registered?

〇 Where are my driver’s license, vehicle registration, or voter registration maintained?

〇 In which country do I hold health insurance or receive social benefits?

〇 Which country have I visited most frequently over the last three years?

3. Trap Two: The “No Tax Residency” Strategy Is Dead After 2025

Many experienced digital nomads used to advocate a strategy of constant movement: avoid staying long enough anywhere to become a tax resident, thereby becoming a kind of “stateless taxpayer” or perpetual traveler.

Ten years ago, this strategy may have existed in a gray area.

In 2025, it has shifted from “high risk” to “almost impossible.”

Why Tax Statelessness No Longer Works

First: CRS and FATCA Closed the Banking Loopholes

Under the Common Reporting Standard (CRS) and FATCA regimes, financial institutions in more than 100 jurisdictions must identify the tax residency of account holders and automatically exchange account information with relevant tax authorities.

If you cannot provide a valid Tax Residency Certificate (TRC), banks may either reject your application entirely or report your information to multiple potentially relevant jurisdictions.

Second: Without Tax Residency, You Lose Treaty Protection

The entire purpose of tax treaties is to allocate taxing rights between two countries and avoid double taxation.

But if no country officially recognizes you as a tax resident, the treaty framework may not protect you at all.

Source countries may apply maximum withholding tax rates to your income, and you may have no legal mechanism to claim relief.

Third: Governments Are Coordinating Against “Double Non-Taxation”

The United Nations Committee on Tax Matters stated clearly in its 2023 report that the greatest risk for digital nomads is not necessarily double taxation.

It is double non-taxation followed by retroactive multi-country enforcement.

As BEPS 2.0 initiatives and global minimum tax frameworks expand, tax authorities are becoming increasingly aggressive toward people who effectively disappear from the tax map.

A Real “Double Enforcement” Example

Marc, a French-Belgian dual citizen and independent consultant, used a “tax statelessness” strategy between 2019 and 2023. He rotated between Portugal, Thailand, and Georgia, spending roughly four months in each country annually.

He never officially declared tax residency anywhere.

He believed that because his clients were global and he never exceeded 183 days in any single country, he had no tax obligations.

In 2024, French tax authorities obtained CRS data showing that his Portuguese bank account held balances exceeding €150,000. Combined with his French birth records and unresolved French social security registration, France concluded that he had never genuinely abandoned French tax residency.

France demanded taxes, penalties, and interest on his worldwide income from 2019 through 2023.

At nearly the same time, Portuguese tax authorities also argued that his Portuguese bank account and rental agreements established Portuguese tax residency for several years.

Marc ultimately had to defend himself in two separate tax investigations simultaneously.

According to his own estimate, the taxes, penalties, and legal fees ultimately exceeded by more than double the taxes he originally believed he had “saved.”

4. Trap Three: Your Apartment May Be Creating a Permanent Establishment for Your Company

This is a trap that most digital nomads — especially freelancers, founders, and remote business owners — barely understand.

What Is a Permanent Establishment (PE)?

In simple terms, if your business activities create a “fixed place of business” in a country, that country may gain the right to tax your company’s profits — even if your company is incorporated somewhere else.

According to the OECD’s updated commentary to the 2025 Model Tax Convention, the standards surrounding remote work and permanent establishment risk are becoming stricter.

Although a major Polish administrative court ruling in 2024 held that “employees working remotely from home do not automatically create a PE,” the critical factor was that the employee had no contracting authority and performed only preparatory or auxiliary activities.

For digital nomads, the danger is different:

You may simultaneously be the employee, director, and decision-maker.

An Overlooked PE Scenario

Tom owned a UK limited company providing digital marketing services.

In 2024, he spent eight months working from an apartment in Barcelona. During that period, he:

- Conducted Zoom meetings with clients from the apartment

- Signed service contracts while physically located in Spain

- Used Spanish internet and telecommunications services

- Opened a Spanish personal bank account to receive some client payments

In early 2025, Spanish tax authorities argued that Tom’s UK company had created a permanent establishment in Spain.

Their reasoning included:

- The Barcelona apartment was a fixed place available for company use

- Tom habitually carried out core business activities there

- He negotiated and concluded contracts while located in Spain

Spain therefore claimed the right to tax the company profits attributable to the Spanish PE at the corporate tax rate of 25%.

Tom’s UK accountant initially assured him that “working from home cannot create a PE.”

But those rules were designed primarily for employees — not for company directors operating businesses remotely.

Tom ultimately had to hire Spanish tax lawyers to defend the case, which remains unresolved.

The Critical Difference

Remote employee working from home ≠ company director operating a business from home.

The second scenario creates far greater PE risk.

5. Trap Four: Exit Tax — The Day You Leave May Become Your Tax Day

This is one of the least discussed — but potentially most expensive — traps in international taxation.

If you come from a country that taxes worldwide income aggressively, leaving the country itself may trigger an immediate tax bill.

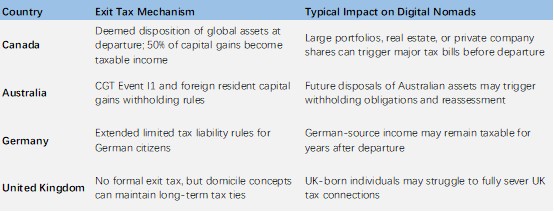

What Is an Exit Tax?

Some countries treat your departure as if you sold all your global assets at fair market value on the day you cease tax residency.

They then immediately tax the unrealized capital gains.

Returning to Sarah’s case:

She held CAD 500,000 in publicly traded shares and CAD 200,000 in private company shares, with a combined cost basis of roughly CAD 400,000.

At departure, the portfolio value was CAD 700,000.

That created CAD 300,000 in unrealized gains.

Under Canadian rules, 50% of those gains — CAD 150,000 — became taxable income in her departure year.

Depending on her marginal tax rate, her departure tax alone could exceed CAD 60,000, excluding her regular employment income for that year.

Another Overlooked Exit Tax Scenario

David, an Australian IT consultant, relocated to Dubai in 2023.

He held approximately AUD 800,000 in Australian publicly traded shares with a cost basis of roughly AUD 300,000.

Friends told him, “Australia doesn’t really have an exit tax — don’t worry about it.”

What he failed to understand was that although Australia’s system differs from Canada’s deemed disposition regime, Australia may still tax gains connected to Australian assets and impose withholding obligations for non-residents.

From January 2025 onward, withholding rules for foreign residents became stricter.

If David eventually sells those investments, his eventual tax burden could actually exceed what he would have paid as a resident.

6. The Solution: Building a “Tax Residency Map” for Digital Nomads

After all these traps, the core question becomes:

If you cannot realistically become “tax stateless,” what should you actually do?

The following framework is based on real-world cross-border experience.

Again, international tax law is highly complex and varies dramatically depending on your personal circumstances.

This article is for informational purposes only and does not constitute tax or legal advice. Always consult qualified professionals familiar with both your home country and destination country before making major decisions.

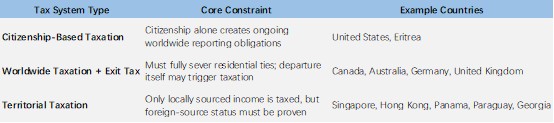

Step One: Understand Your “Tax Origin”

Different citizenship and residency systems create very different obligations.

If You Are American

Leaving the U.S. does not mean leaving the IRS.

The Foreign Earned Income Exclusion (FEIE) may reduce federal income tax obligations, but self-employment tax (Social Security + Medicare = 15.3%) often still applies unless you establish sufficient social security ties in a treaty country.

An American freelancer earning USD 85,000 annually may reduce federal income tax to zero under FEIE while still owing roughly USD 12,000 in self-employment taxes.

If You Are Canadian, European, or Australian

Your primary priority should be properly executing a formal tax departure process — not simply buying a plane ticket.

Step Two: Intentionally Choose a Primary Tax Residency Country

Do not attempt to become a “tax resident of nowhere.”

Instead, intentionally choose a favorable primary tax residency jurisdiction and obtain a Tax Residency Certificate (TRC).

Criteria for Choosing a Primary Tax Residency Country

1. A tax system compatible with your income structure

2. Realistic physical presence requirements you can actually satisfy

3. Administrative practicality, including access to TRCs and banking

4. A country where you genuinely want to live — not purely a paper solution

Real Choices Some Digital Nomads Are Making in 2025

- United Arab Emirates (UAE): 0% personal income tax, but requires meaningful physical presence

- Portugal: Historically attractive under the NHR regime, though rules tightened after 2024

- Georgia: Certain IT freelancers may qualify for approximately 1% taxation under small business structures

- Croatia: Some digital nomad visa holders may qualify for exemptions on foreign-source income

Step Three: Execute a Real Tax Severance

The following is a general departure checklist based on international practice. Requirements vary significantly by country.

Legal and Administrative Actions

〇 Officially deregister residency

〇 Cancel or update voter registration and driver’s licenses

〇 Sell or convert primary residences into purely investment properties

〇 Update bank accounts to non-resident status

Economic and Social Ties

〇 Cancel gym memberships, clubs, and local associations

〇 Update addresses for investment accounts, insurance, and pensions

〇 Redirect mail properly

〇 Establish healthcare and social ties in the new country

Evidence Preservation

〇 Keep departure records and boarding passes

〇 Retain lease termination documents

〇 Obtain Tax Residency Certificates from the new jurisdiction

Step Four: Build a “Mobility Log” System

This is not merely for tax audits.

It is for helping you understand your own exposure and provide accurate information to tax professionals.

One Practical Tip

Enable GPS location history on your phone.

This is not about sharing your location publicly.

It is about being able to prove, if necessary, that on March 15, 2024, you were physically in Singapore and not in Canada.

7. Common Misconceptions

These misunderstandings appear repeatedly among digital nomads worldwide.

❌ “A digital nomad visa means tax-free status”

✅ Visas and tax systems are completely separate issues.

Many digital nomad visas only legalize your stay. They do not provide tax exemptions and may even require local tax residency.

❌ “I stay in Airbnbs, so I don’t have a permanent home”

✅ Tax authorities care about whether accommodation is “available for your use,” not ownership.

A six-month Airbnb rental in Lisbon may absolutely qualify as a permanent home.

❌ “My clients are American, so I only owe U.S. tax”

✅ If another country considers you a tax resident, it may have primary taxing rights over your worldwide income.

Tax treaties, foreign tax credits, and FEIE mechanisms only help if everything is properly reported.

❌ “Small income amounts won’t trigger scrutiny”

✅ Under CRS reporting, banks report balances and flows automatically.

From an information-sharing perspective, USD 10,000 and USD 1 million are both reportable data points.

❌ “My accountant said everything was fine”

✅ Many accountants only understand domestic tax law.

If your advisor lacks international tax experience, their advice may completely ignore foreign tax rules.

Seek professionals with genuine cross-border expertise.

Appendix: Additional Reading and Tools

Official Resources

- OECD Model Tax Convention and Commentary (2025 Update)

- United Nations Committee of Experts on International Cooperation in Tax Matters — Digital Nomad Taxation Report (2023)

- Official tax residency guidance published by relevant national tax authorities

Practical Tools

- Travel tracking tools such as TravelSpend, Nomad List, or simple spreadsheets

- OECD Tax Treaties Database

Important Disclaimer

This article is based on publicly available information, practical observations, and discussions within the global digital nomad community.

Tax law varies significantly depending on your citizenship, residency history, destination country, asset structure, and timeline.

Always consult licensed tax and legal professionals before making decisions related to residency, international relocation, or taxation.

FAQs

1. Can I legally avoid tax residency by staying under 183 days in every country?

Not necessarily. Many countries use additional tests beyond physical presence, including permanent home availability, center of vital interests, habitual abode, economic ties, and family connections. Staying under 183 days may reduce risk, but it does not automatically prevent tax residency.

2. What happens if two countries both claim I am a tax resident?

In that situation, tax treaties may apply “tie-breaker rules” to determine which country has primary residency rights. These rules often consider where your permanent home is located, where your family lives, and where your strongest economic and personal ties exist.

3. Is it possible to become completely “tax-free” as a digital nomad?

For most people, no. Modern international reporting systems such as CRS, FATCA, and cross-border banking compliance make it increasingly difficult to remain outside all tax systems simultaneously. Most experienced international tax professionals now recommend establishing a legitimate primary tax residency instead.

4. Do digital nomad visas provide tax exemptions?

Not automatically. Most digital nomad visas primarily address immigration status and legal stay rights. Tax obligations are usually determined separately under domestic tax law and tax treaties.

5. How can digital nomads reduce tax residency disputes?

Common strategies include establishing a clear primary residency country, maintaining organized travel records, formally severing ties with previous jurisdictions, and consulting experienced cross-border tax professionals before relocating.

References

1. Organisation for Economic Co-operation and Development. (2025). OECD Model Tax Convention on Income and on Capital: Condensed Version. OECD Publishing.

2. United Nations Committee of Experts on International Cooperation in Tax Matters. (2023). Tax Challenges Related to Digital Nomads and Remote Work Arrangements. United Nations.

3. Canada Revenue Agency. (2025). Emigrants and Income Tax. Government of Canada.

4. Internal Revenue Service. (2025). Substantial Presence Test. U.S. Department of the Treasury.

5. Australian Taxation Office. (2025). Foreign Resident Capital Gains Withholding. Government of Australia.

6. HM Revenue & Customs. (2024). Residence, Domicile and the Remittance Basis. Government of the United Kingdom.

7. European Commission. (2024). Taxation and Customs Union: Cross-Border Tax Issues in the Digital Economy. European Union.

8. KPMG International. (2025). Digital Nomad Taxation and Remote Work Trends Report. KPMG.

9. PwC. (2025). Managing Permanent Establishment Risk in the Era of Remote Work. PricewaterhouseCoopers.

10. Deloitte. (2024). International Tax Guide for Globally Mobile Individuals. Deloitte Insights.

About the Author

Marco Elian Ruiz

Marco Elian Ruiz is a remote work strategist and former freelance consultant who has spent years working across Southeast Asia, Southern Europe, and Eastern Europe while advising independent professionals and distributed teams. His writing focuses on the economics of remote work, digital nomad culture, freelance sustainability, and geographic arbitrage. Marco is particularly interested in the gap between the marketed “freedom lifestyle” and the operational realities of online work, including taxation, client dependency, unstable income cycles, and long-term career resilience for remote workers.

Editorial Transparency Statement

This article was independently researched and written using publicly available materials, including official government publications, OECD guidance, international tax reports, and professional commentary related to digital nomad taxation and remote work compliance.

The content is intended for educational and informational purposes only. No government agency, tax advisory firm, financial institution, or immigration service sponsored or influenced this article. Examples and scenarios included in the article are based on commonly reported international tax situations and may combine multiple real-world patterns for educational clarity.

Tax laws, reporting obligations, residency rules, and treaty interpretations can change frequently and vary significantly depending on individual circumstances. Readers are encouraged to verify all information through official government sources and qualified professionals before making financial, immigration, or tax-related decisions.

Disclaimer

The information contained in this article does not constitute legal, tax, accounting, immigration, or financial advice. International tax law is highly complex and depends on many individual factors, including citizenship, residency history, income sources, asset ownership, corporate structures, and applicable tax treaties.

Readers should not rely solely on this article when making decisions related to relocation, tax residency, business structuring, or international financial planning. Always consult licensed tax professionals, qualified legal advisors, or certified cross-border specialists familiar with the laws of the relevant jurisdictions before taking action.

Although reasonable efforts were made to ensure accuracy at the time of publication, no guarantee is made regarding completeness, timeliness, or applicability to any specific individual situation.